Increase in the basic personal deduction

The new gross minimum wage automatically raises the maximum limit for the basic deduction to 865 lei.

READ MORE

Starting July 1, the tax-exempt portion of the minimum wage will decrease to 200 lei, reducing real take-home pay, but the gross income threshold for eligibility for the tax break will increase to 4,600 lei.

Read article

The Romanian labor market is entering a new phase of tax recalibration starting in the summer of 2026. The tax relief that allowed a portion of the minimum wage to be tax-exempt will change as of July 1, 2026: the tax-exempt amount will decrease from 300 lei to 200 lei for the period July 1–December 31, 2026. The measure comes alongside a provision intended to mitigate its impact: the maximum gross income threshold up to which this exemption applies will increase from 4,300 lei to 4,600 lei. These provisions are set forth in Article 3 of Government Emergency Ordinance No. 89 of December 23, 2025.

What exactly does this measure entail?

The new regulation revises this benefit in two ways:

Who is eligible for the 200 lei tax-free allowance?

To qualify for this tax exemption, all of the following conditions must be met:

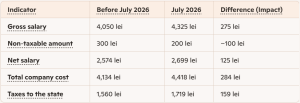

How does this change affect your wallet?

To fully understand the pricing mechanism, we need to assess the cumulative impact. A direct comparative analysis shows us how the amounts received by the employee change in relation to the company’s total financial outlay.

Starting in July 2026, although gross pay will increase by 275 lei, only 125 lei will actually end up “in your pocket,” with the remaining 159 lei going to the government in the form of taxes.

The new gross minimum wage automatically raises the maximum limit for the basic deduction to 865 lei.

READ MORE

Although Romania missed the deadline without actually adopting the law transposing the EU directive, pay transparency is rapidly becoming the new reality in HR.

READ MORELegal Risks and Obligations Related to the Use of Artificial Intelligence Systems.

READ MORE